Covid-19 Special NRS Pay Point of Sale Pricing: $699 (REG. $1299)

Covid-19 Special NRS Pay Point of Sale Pricing: $699 (REG. $1299)

Key Takeaways

Table of Contents:

A payment API is a set of protocols that allow different software systems to communicate and process financial transactions online. Think of it as a digital bridge that connects your website or app to the banking world. I’ve spent over a decade implementing these systems, and trust me, they’re the unsung heroes of online commerce.

Payment APIs facilitate the secure transmission of sensitive payment data between customers, merchants, and financial institutions. They verify card details, check for fraud signals, and confirm sufficient funds—all in seconds!

Different types of payment APIs exist to serve various business needs:

These APIs vary in complexity and features, but they all share one core purpose: making online payments possible. Without them, businesses would still be mailing checks or using cash for everything! NRSPay offers several API solutions designed specifically for businesses at different growth stages.

The backbone of any payment API is its security infrastructure. This isn’t just some optional extra—it’s absolutely critical. Payment APIs use multiple security technologies:

Authentication in payment APIs works on multiple levels:

| Authentication Type | Purpose | Example |

| User Authentication | Verifies the customer’s identity | Two-factor authentication |

| Merchant Authentication | Confirms the business is legitimate | API keys, OAuth tokens |

| Transaction Authentication | Validates each payment request | 3D Secure, CVV verification |

Each layer adds protection while maintaining a balance with user experience. The challenge has always been finding that sweet spot where security doesn’t create too much friction for users.

Payment APIs process several types of data during a transaction:

The environmental impact of all this digital processing is actually quite interesting. Most people are unaware that digital payments have a significantly smaller carbon footprint compared to traditional cash and check processing systems.

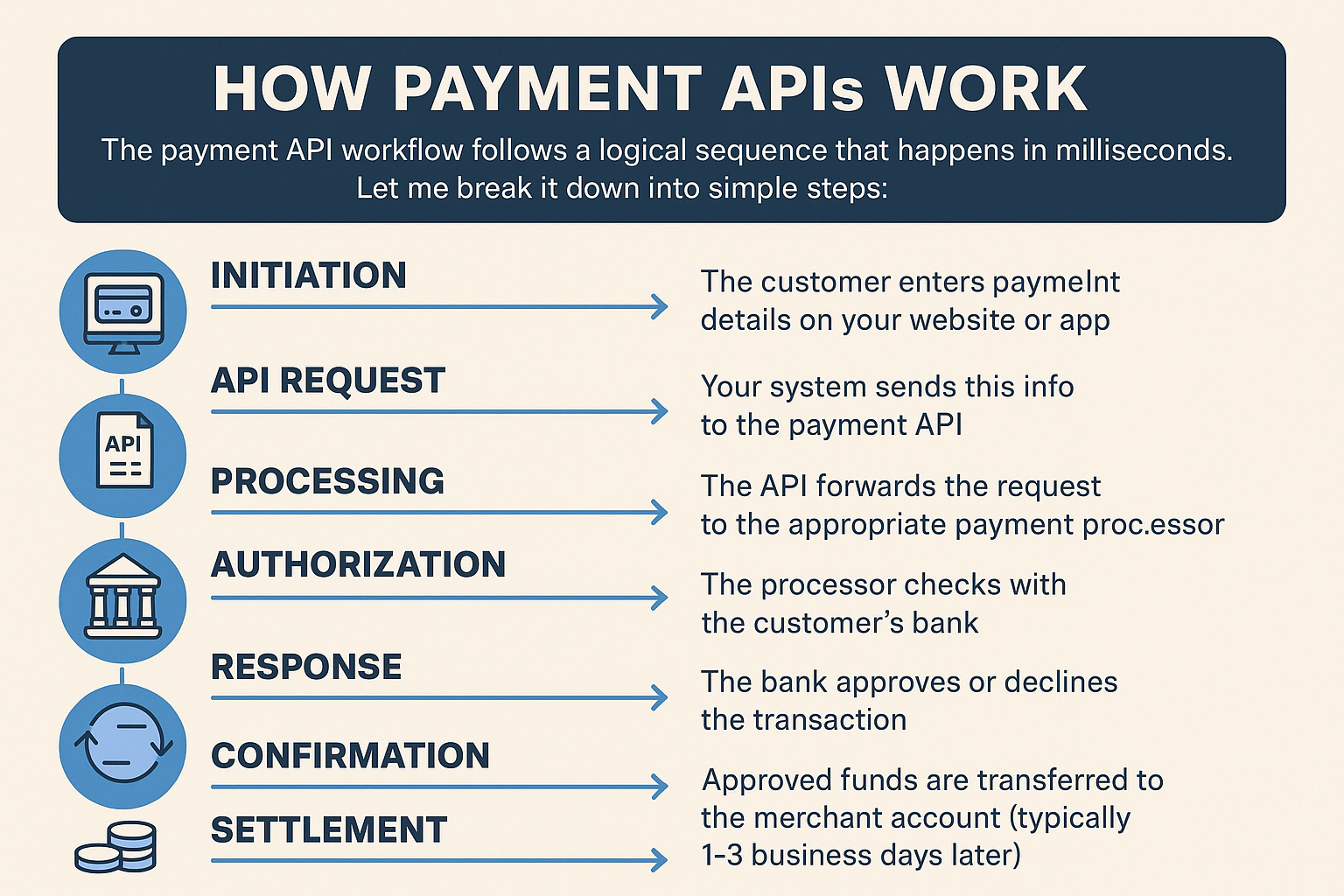

The payment API workflow follows a logical sequence that happens in milliseconds. Let me break it down into simple steps:

This process has to be lightning-fast. In my experience, customers start abandoning carts if authorization takes more than 5 seconds! Modern payment APIs typically complete the authorization steps in under 2 seconds.

One of the really cool things about payment APIs is how they handle various payment methods. Whether a customer uses Visa, Mastercard, PayPal, or Apple Pay, the API translates all transactions into a standardized format that your systems can understand. For businesses looking to implement e-commerce credit card processing, choosing the right API is crucial for supporting multiple payment options.

Payment APIs offer robust security that would be extremely difficult for individual merchants to develop independently:

The impact of payment APIs on customer experience can’t be overstated:

Research consistently shows that the checkout experience has a direct impact on conversion rates. A study revealed that businesses that enhance their credit card customer experience achieve up to 27% higher conversion rates.

Payment APIs offer significant advantages for businesses:

The scalability aspect is particularly important for growing businesses. Some startups transition from 50 transactions per day to 10,000+ without modifying their payment infrastructure, simply because they chose a scalable API from the outset.

Implementing a payment API requires several technical components:

The good news? Payment API providers have simplified this process significantly over the years. What used to take months can now often be completed in weeks or even days.

Based on my experience with dozens of implementations, here are the key best practices:

Common challenges during payment API integration include:

These challenges aren’t insurmountable, but they require planning and patience. The integration process is getting easier as more providers adopt modern, RESTful API designs and improve their documentation.

The shift to contactless payment technology has added another layer of complexity, but it has also created opportunities for businesses implementing payment APIs.

The payment API landscape is evolving rapidly with several exciting developments:

Embedded Finance is already changing how we think about payments—why switch to a banking app when your shopping app can handle the transaction directly?

Open banking initiatives are fundamentally changing payment APIs:

This shift represents both opportunities and challenges. More competition means better services, lower fees, and a more complex landscape to navigate. Effective community management among developers and API providers has become crucial for staying current with these rapid changes.

Regulations continue to shape payment API development:

Staying compliant with these evolving regulations is challenging but essential. The most successful payment API implementations build compliance into their foundation rather than treating it as an afterthought.

Payment APIs have transformed online commerce from a risky, complicated endeavor into something we now take for granted. They handle the complex dance between customers, merchants, processors, and banks with remarkable efficiency and security.

For businesses, implementing the right payment API isn’t just a technical decision—it’s a strategic one that impacts customer satisfaction, security posture, and operational efficiency. The initial investment in proper integration pays dividends through higher conversion rates, reduced fraud losses, and valuable business insights.

As we move into an increasingly cashless future, payment APIs will continue to evolve, supporting new payment methods and adapting to changing regulations. The businesses that prosper will be those that view their payment infrastructure not as a mere utility but as a competitive advantage.

The future of commerce is digital, and payment APIs are the foundation that makes it possible. By understanding how they work and implementing them effectively, businesses can position themselves for success in the rapidly evolving payment landscape.

Payment APIs work as digital intermediaries that securely transfer payment data between your website or app and financial systems. They send encrypted transaction information to payment processors, which communicate with banks to verify and complete transactions. The entire process occurs in seconds, enabling real-time payment authorizations while safeguarding sensitive financial data.

Payment APIs can process transactions, securely store payment methods, handle recurring billing, convert currencies, detect fraud, generate receipts, reconcile accounts, and provide analytics. They support multiple payment methods, including credit cards, digital wallets, and bank transfers, all through a single integration point that simplifies the complex world of financial transactions.

When selecting a payment API, consider security certifications (PCI DSS compliance), supported payment methods, fee structure, geographical coverage, integration complexity, documentation quality, testing tools, scalability, customer support quality, and downtime history. Also, evaluate fraud protection features and whether the API provides useful analytics and reporting tools for business insights.

Easy integration reduces development time and costs while minimizing the risk of errors that could lead to payment failures or security vulnerabilities. A user-friendly API with clear documentation allows for faster implementation, quicker troubleshooting, and easier maintenance. This directly impacts time-to-market for new features and your team’s ability to adapt to changing payment requirements.

Payment APIs typically offer several integration methods, including direct API integration (RESTful or SOAP), hosted payment pages, mobile SDKs for iOS and Android, and pre-built plugins for popular e-commerce platforms like Shopify, WooCommerce, and Magento. The best choice depends on your technical resources, security requirements, and how much control you need over the payment experience.

By Darya Furs